By Dr Arkadius Sybaris

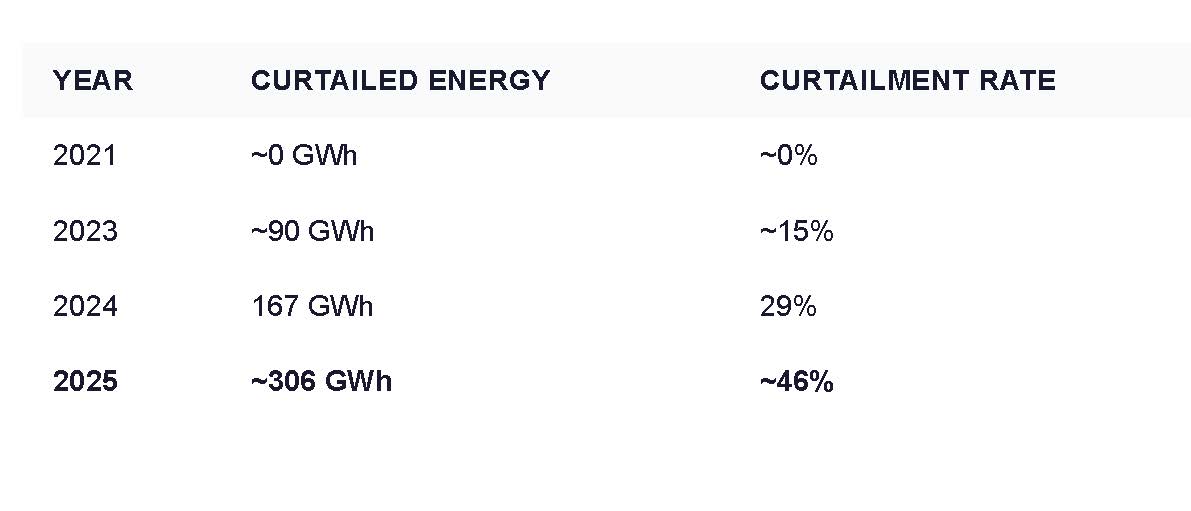

In 2025, Cyprus curtailed an estimated 306 gigawatt-hours of clean solar energy — enough to power roughly 51,000 homes for a year. Approaching half of all distributed solar generation on the island was produced and then thrown away because the grid could not absorb it. Meanwhile, the island’s electricity sector spent an estimated €250–350 million on EU carbon allowances — the price of continued dependence on fossil fuel generation. Battery storage technology can help address both problems. So where do things stand?

The numbers behind the waste

Four years ago, solar curtailment in Cyprus was essentially zero. By 2024 it had reached an estimated 29%. In 2025, industry estimates put it at approaching 46 per cent — nearly doubling in a single year. Every new rooftop installation makes it worse, because the island has no way to store the midday surplus and no interconnection to export it.

To put that in perspective: 306 GWh is more energy than the entire city of Paphos consumes in a year. It was generated cleanly, at no fuel cost, and discarded.

The reason is structural. Cyprus operates the only fully isolated electricity grid in the European Union. Unlike Greece, which connects its islands via submarine cables to the mainland, or Ireland, which shares interconnectors with Great Britain, Cyprus has no electrical link to any other country. When solar output exceeds demand at midday, there is nowhere for the surplus to go.

What battery storage would change

Battery energy storage systems — large containerised installations co-located with solar parks — capture surplus solar energy during the midday peak and discharge it during the evening, when demand is highest and electricity prices spike.

The economics are compelling. Data from the Cyprus Transmission System Operator’s Day-Ahead Market covering 134 consecutive days (October 2025 to February 2026) shows a consistent daily price pattern: midday wholesale prices average €101 per megawatt-hour, while evening peak prices average €183. On every single one of those 134 days, the spread was positive. There was not a single day when storing solar energy and releasing it later would have lost money.

For a typical 5 MW solar park adding a 20 MWh battery system, the annual revenue from recovering curtailed energy alone is approximately €294,000. The system pays for itself within six to nine years and continues generating revenue for a further decade.

Progress — and what remains

The good news is that things are moving. Since January 2026, Cyprus has opened the door for solar park operators to install battery storage systems alongside their existing plants. This is a welcome and significant step — it means park owners can finally begin recovering the curtailed energy that has been costing them hundreds of thousands of euros per year. Several operators have already placed orders for battery equipment, and the first installations are expected later this year.

Credit is due to CERA and the DSO for establishing the Category B framework that makes this possible. It is a meaningful beginning.

But the framework remains incomplete compared to what exists across the rest of the EU. Battery storage in Cyprus still cannot participate as a buyer in the electricity market — meaning operators cannot purchase cheap surplus power from the day-ahead market and sell it during peak hours, as they can in Germany, Spain, Italy, Greece, Portugal and the Netherlands. Category B systems cannot charge from the grid at all, only from their co-located solar panels. And software-based power limiting — a standard, cost-effective practice encouraged across Europe — is not permitted.

These are not criticisms of the progress made. They are an indication of how much further the framework needs to develop to reach the European standard — and how much additional value could be unlocked for park owners, consumers, and the grid itself once it does.

Scale matters

The TSOC’s planned 120 MW / 400 MWh battery installation, partly funded by the EU Just Transition Fund, will be an important addition to the island’s infrastructure. But it cannot address the challenge alone. Thirty-three private companies hold BESS licences in Cyprus representing over 1,000 MW of potential capacity. Enabling these private investments alongside the TSOC system — rather than sequentially — would accelerate deployment and distribute the grid stability benefits across the island far more quickly.

The opportunity is to build a storage ecosystem, not a single installation. That requires giving private operators the same market access that their counterparts enjoy across Europe.

“We are now entering a European BESS cycle. The first wave of solar and wind installations has reached the technical limits of what existing grids can accommodate. Battery storage is the necessary intermediate phase that enables the next wave of clean generation. Cyprus cannot afford to sit this out.”~ Dr Arkadius Sybaris

What it costs you

The consequences of inaction are not abstract. They appear on every electricity bill in Cyprus.

Cyprus’ electricity sector pays an estimated €250–350 million per year in EU Emissions Trading System allowances — among the highest per capita in the EU. Much of this is driven by the continued reliance on fossil fuel generation, including must-run thermal units that the TSO requires for grid inertia even when solar could meet demand. Curtailment contributes directly: every megawatt-hour of wasted solar that gets replaced by fossil generation adds to the carbon bill. The cumulative ETS cost from 2018 to 2025 is estimated at approximately €1.28 billion. These costs are socialised — passed through to every consumer via regulated tariffs.

Other island and isolated grid systems have found ways to reduce this burden. Ireland’s DS3 programme, operational since 2016, used battery storage to cut must-run thermal generation from roughly 50 per cent to 20 per cent. Germany launched a dedicated inertia services market in January 2026, paying storage operators €8,000–17,000 per MW per year. The UK has deployed over 12.5 GW of battery storage through its Stability Pathfinder programme.

Cyprus has no equivalent mechanism. Battery storage cannot compete with thermal plants for grid stability contracts, because no such contracts exist for storage.

A security question, not just an economic one

Recent events have made the vulnerability of Cyprus’s energy infrastructure impossible to ignore. The drone strikes across the region are a reminder that centralised, fuel-dependent power systems are exposed in ways that decentralised grids are not.

“Vasilikos power station depends on imported fuel. Any sustained supply disruption — whether from regional instability, shipping delays, or sanctions — would put pressure on generation capacity,” says Alexander Papacosta, Managing Director of Lighthief Cyprus & Greece. “The more generation the island can source from domestic renewables backed by storage, the less exposed it is to fuel supply risk. A decentralised grid is not just cleaner and cheaper — it is more resilient.”

In EU markets with mature grid codes, battery storage provides automatic frequency containment reserves (FCR) and automatic frequency restoration reserves (aFRR) — fast-response stability services that keep the grid running when generation or demand shifts suddenly. These are the same services that protect grids during emergencies. Cyprus has no market mechanism for either.

The equipment to provide these services already exists on the island. Several Cyprus solar park operators have ordered battery systems with grid-forming inverter capability — hardware that can independently stabilise voltage and frequency without relying on a central power station. But without a TSO framework allowing storage to offer stability services, that capability sits unused.

“We are not talking about future technology,” Papacosta adds. “Grid-forming battery systems are deployed across Europe today. The hardware is ordered. What Cyprus lacks is the regulatory permission to switch it on.”

The path forward

The technical challenge is real. An isolated grid with 1,500 MW of peak demand and no interconnections requires careful management. But the solutions deployed across Europe — from Crete to the Canary Islands to Ireland — demonstrate that island grids and battery storage are not incompatible. They are, in fact, the strongest possible match.

Building on the positive steps already taken, three further developments would bring Cyprus in line with the European standard: allowing storage to participate in the day-ahead market as both buyer and seller; creating ancillary services markets — FCR and aFRR — where storage can provide grid stability alongside conventional generation; and permitting grid-forming battery systems to deliver the inertia services that currently only fossil fuel plants can offer.

None of these are untested ideas. They are operational reality in every comparable EU market. Cyprus has taken the first step by enabling curtailment recovery. The next steps would unlock the full value of battery storage — for park owners, for consumers, and for the resilience of the island’s grid.

“The successful implementation of energy storage in Cyprus requires not only the right technology but also the operational expertise gained from deployment across European markets. Our teams in Poland, Italy, and Spain — reinforced by engineers from our international manufacturing partners — have already solved the integration problems that Cyprus hasn’t yet faced. The technical knowledge exists. What’s needed now is the regulatory space to apply it.” ~ Alexander Papacosta, Managing Director, Lighthief Cyprus & Greece

About Lighthief energy group

Dr Arkadius Sybaris is the founder of Lighthief International, a renewable energy group operating across 11 European nations. Lighthief Cyprus manages a portfolio of battery storage projects totalling 249 MW / 882 MWh across 51 licensed solar parks on the island. Alexander Papacosta is the Managing Director of Lighthief Cyprus & Greece.

Disclosure: The authors have a commercial interest in battery storage deployment in Cyprus. All market data cited is from public TSOC Day-Ahead Market reports. Curtailment and ETS figures are industry estimates based on published sources.

Data sources: TSOC Day-Ahead Market reports (134-day dataset, October 2025 – February 2026); CERA; DSO Technical Guide for Storage, Edition 2025.1 (EAC); EU Directive 2019/944; Law N.130(I)/2021; Poullikkas, A. (2026), Energies 19(1); Kathimerini Cyprus (ETS cost data); regulatory analysis based on primary legislation from 14 EU member states.

Contact:

Alexander Papacosta — [email protected] — +357 99 164 158

Dr. Arkadiusz Sybaris — [email protected] — +357 95 152 788

Web: solarfarms.cy | lighthief.cy

Click here to change your cookie preferences